-

Commercial Real Estate

Capitalize on opportunities and prepare for challenges throughout the real estate cycle.

-

Consumer and Retail

We’re here to help you adapt to the rapidly changing environment with end-to-end solutions. Whether you’re exploring new commerce models, adapting your physical stores or managing supply chains, J.P. Morgan powers consumer and retail organizations to support strong business models.

-

Diversified Industries

J.P. Morgan delivers world-class financial solutions to clients across industries. From aerospace and defense, industrials to basic materials, transportation to automotive, we can help drive new possibilities for your business.

-

Energy, Power and Renewables Financial Solutions | J.P. Morgan

J.P. Morgan offers cutting-edge banking and finance solutions to clients in energy investment, utilities, renewable resources, power infrastructure and beyond.

-

Financial Institutions

Leverage our global expertise in financial services to support your business goals and objectives, including corporate lending, capital raising and risk management.

-

Health Care

Adapt to the fast-paced health care landscape to deliver quality care. Whether you’re a provider, researcher, manufacturer or startup, J.P. Morgan powers health care organizations with solutions to build financial strength, resiliency and growth.

-

Media, Telecom and Entertainment

We're hard at work behind the scenes to help media and entertainment companies—from film and music to streaming and gaming.

-

Public Sector

Serve your communities effectively with public sector financial solutions built to adapt and scale. Our experts understand the unique needs of public sector organizations, including government agencies, government sponsored entities and supranationals.

-

Technology

The technology sector continues to change at a rapid pace. As a partner, we can work with you to solve challenges around resource constraints, fragmented solutions, and friction in user experience.

Client stories

Banking

Apr 11, 2024

Startups to multinational enterprises rely on Rippling to run their businesses, and most important, their payroll. Find out how J.P. Morgan and Rippling worked together to get money moving when it mattered the most.

Read more

Banking

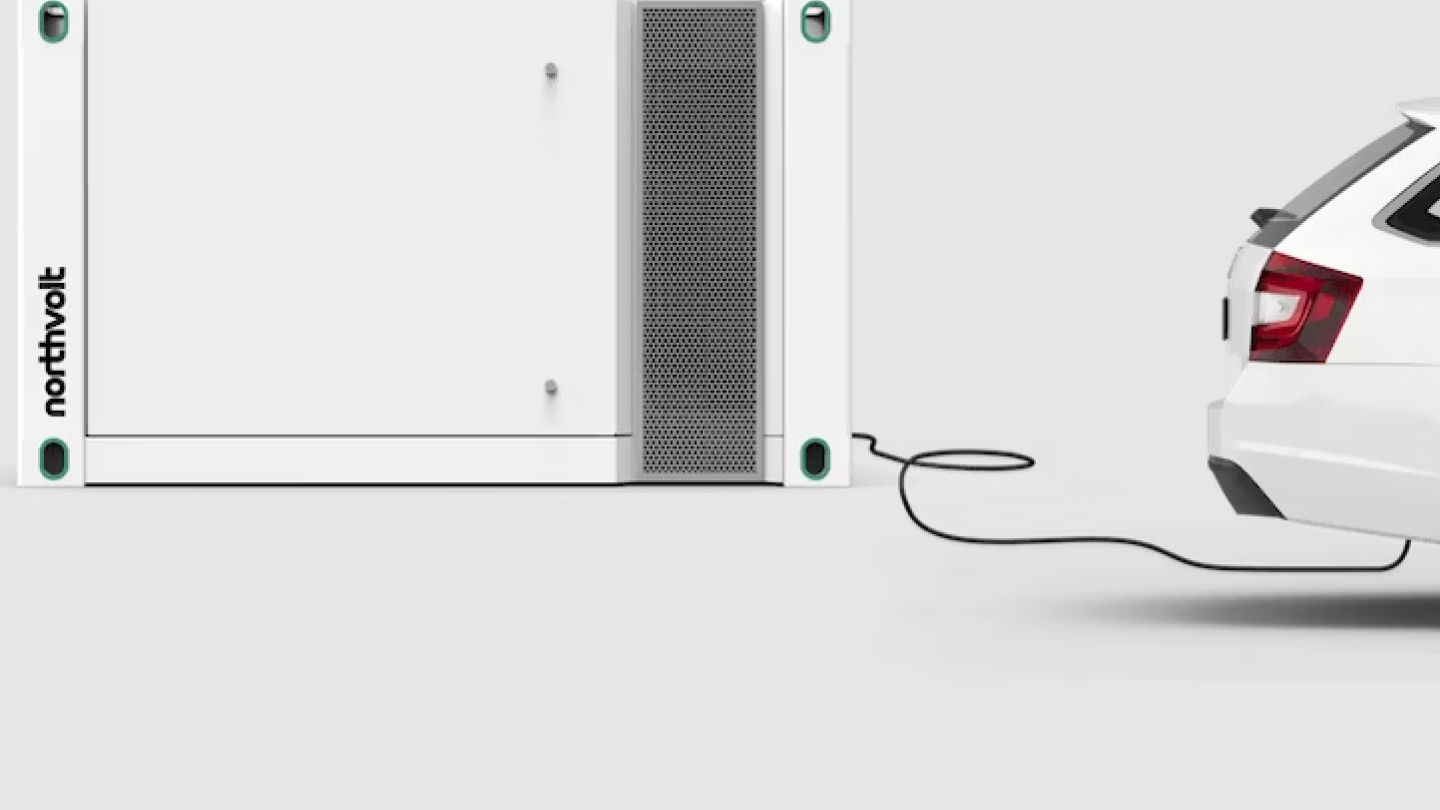

A $5 billion supercharge for battery maker Northvolt

Feb 27, 2024

J.P. Morgan recently supported Europe’s largest ever green loan amid booming investor appetite for sustainable finance.

Read more3:56 - Corporate Responsibility

For these business leaders, impact and legacy go hand in hand

Watch videoRelated insights

Real Estate

What you need to know before buying a luxury home

Apr 18, 2024

It’s no bubble. Luxury home prices are rising for good reasons – and you can still find good value.

Read more

International

Trends in European venture capital

Apr 18, 2024

Our experts discuss the trends affecting the European venture ecosystem in the first quarter of 2024, including the state of IPO and private capital markets, macroeconomic and political impact, and where things stand one year after market disruption.

Read moreGet in touch

Hide

Get in touch

Hide