Commercial Banking solutions

Commercial Banking solutions

Commercial Banking products

Chase Connect®

Connect to all your accounts through one unified, easy-to-navigate portal. Get your loans, cards and merchant services accounts in one place with Chase Connect®.

Commercial cards

Our commercial card program can help your employees spend less time authorizing, tracking and processing expense data.

Digital Bill Payment

Digital Bill Payment is an innovative bill presentment and payments solution that grows with your business.

Rent solutions

Whether you’re a national real estate developer, affordable housing operator or local investor, we can help you streamline your online rent payments.

Who we serve

From startups to legacy brands, you're making your mark. We're here to help.

Innovation economy

JPMorgan Chase has the expertise and financial solutions to support your business from early stage to IPO— and everything in between.

Midsize businesses

Seize growth opportunities with our custom banking solutions and global resources designed for middle market businesses and specialized industries.

Large corporations

From complex operations to global competition, we’re here to help. Leverage the power of JPMorgan Chase to solve your business challenges.

Commercial real estate

Get the strategic support to be successful throughout market and real estate cycles with insights, hands-on service, comprehensive financial solutions and unrivaled certainty of execution.

Industries

Our commercial and investment banking specialists draw on their expertise across industries to help manage your finances and grow your business.

100+

Countries where Commercial Banking operates

~55K

Number of Commercial Banking clients

Latest client stories

Corporate Responsibility

For these business leaders, impact and legacy go hand in hand

Feb 20, 2024

With a mission to uplift others and leave a positive mark on the world, BCforward’s Justin and Darrianne Christian are building an IT powerhouse and inspiring students at their alma mater.

Watch video

Banking

J.P. Morgan and Rippling

Apr 11, 2024

Startups to multinational enterprises rely on Rippling to run their businesses, and most important, their payroll. Find out how J.P. Morgan and Rippling worked together to get money moving when it mattered the most.

Read more

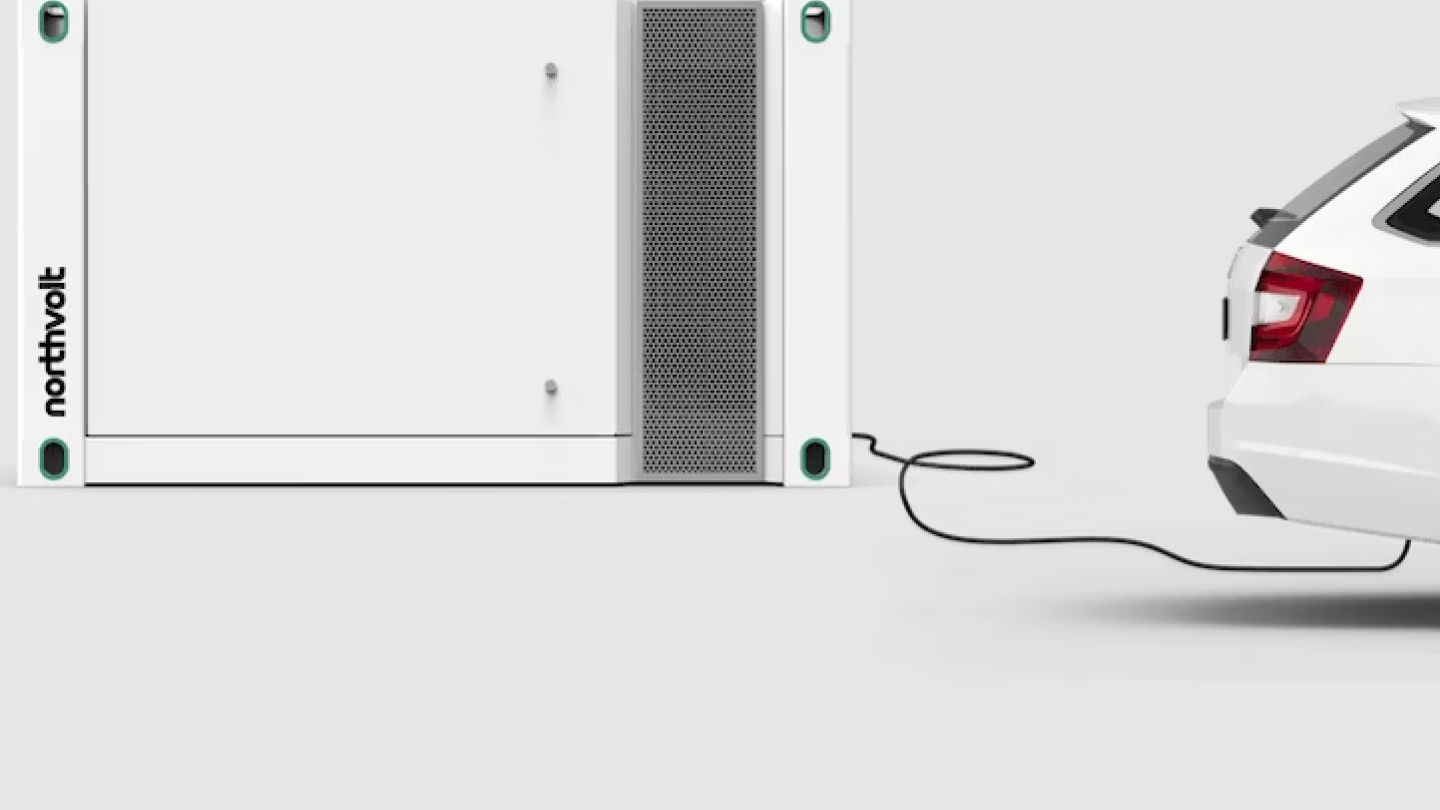

Banking

A $5 billion supercharge for battery maker Northvolt

Feb 27, 2024

J.P. Morgan recently supported Europe’s largest ever green loan amid booming investor appetite for sustainable finance.

Read more3:56 - Corporate Responsibility

For these business leaders, impact and legacy go hand in hand

Watch videoLatest insights

Business

How to stay nimble and innovate through uncertainty

Apr 16, 2024

Ann Ramakumaran explains her approach to business resiliency and scaling over 20 years of growth.

Watch video

Retirement

3 ways to stay active while in retirement

Apr 16, 2024

Staying active in retirement is important. Here’s how you can stay energized, put your expertise to use and keep your finances in check in retirement.

Read more

Wealth Planning

Four mistakes with life insurance you don’t need (or want) to make

Apr 16, 2024

Purchasing life insurance can feel overwhelming, but following these guidelines can make this important decision on your family’s future well-being more straightforward.

Read more

Take a closer look

Take a closer look

Our impact

Discover how we help strengthen communities.

Our newsletters

Access economic and industry insights.

Our podcasts

Hear discussions on research, treasury and more.

Transacting with us

Use these methods to initiate financial transactions when your primary methods are unavailable.

News and announcements

Keep up with what's happening at JPMorgan Chase.

Contact us

Our team can answer questions and provide more information.